Govt’s own modelling shows LNG leads to higher electricity prices than other solutions

19 Feb 2026

By Christina Hood

COMMENT: According to modelling conducted by Concept Consulting for MBIE, either developing the Tariki gas storage facility or managing electricity demand would deliver lower wholesale electricity prices than the Government’s preferred solution of an LNG import terminal.

And that’s even when the modelling has made LNG prices look artificially low, because the LNG import terminal’s fixed costs are subsidised in all scenarios via a levy on electricity consumers.

Last week, the Government announced it would rush to build an LNG import terminal to tackle New Zealand’s ‘dry year risk’. The Government claims its plan will reduce prices for consumers, however there are serious flaws and omissions in the government’s numbers.

Key alternatives were not considered

The Government chose not to seriously assess other ways of closing the dry-year energy gap: only LNG was modelled in detail. Other alternatives like accelerating renewables and storage, demand response, a coal/biofuel plant or diesel peakers were either dismissed entirely or only given a cursory treatment. The brief assessment of a biomass pellet plant actually showed a stronger potential impact on lowering electricity prices and had significant economic benefits, but was rejected because it is a long-term, not a temporary “flexible”, solution. That illustrates that the criteria used were very narrow, and as a result may well have ignored better options.

Gas storage

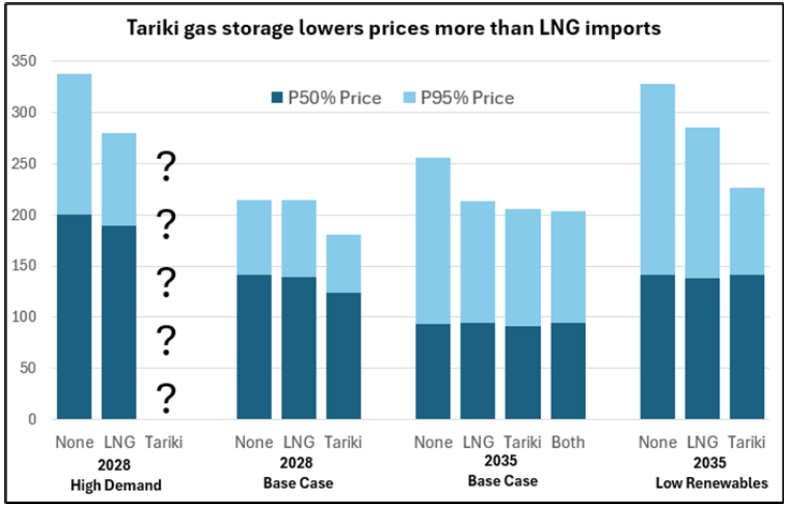

The modelling shows that developing the Tariki gas storage facility lowers electricity prices more than the government's LNG plan. The Tariki project being developed by Genesis Energy and partners would provide up to 10PJ of storage, which is a similar magnitude to the government’s sizing of 12PJ of LNG needed in a dry winter.

Among the scenarios modelled for MBIE by Concept Consulting, there were three groups of scenarios with the same underlying assumptions, where a like-for-like comparison is possible between no-intervention, LNG only, or Tariki only – these are the three groupings on the right in the graph below. Note that the prices shown are only the modelled wholesale prices, and do not add the proposed $2-$4/MWh levy for LNG fixed costs.

Tariki (unsubsidised) performs better than LNG (with levy subsidy) in each example where a like-for-like comparison can be made. There is also one set of scenarios where there is also a variant with both Tariki and LNG: here adding LNG once Tariki is in place makes no substantial difference to electricity prices.

|

| IMAGE: Christina Hood |

Frustratingly, MBIE chose to use a "High Demand" scenario for 2028 rather than Concept Consulting’s baseline in their advice to ministers, and there was no “with Tariki” variant modelled. MBIE’s advice to the minister was therefore that LNG (if subsidised via levy) makes electricity prices cheaper, but they didn’t even model the obvious zero-cost alternative. In my view that is negligent, given the $1 billion plus commitment of consumers’ money at stake.

Demand management

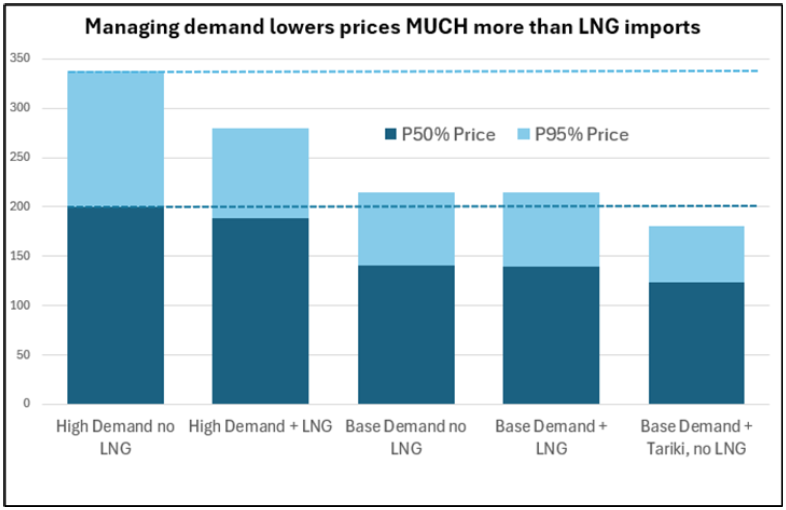

The modelled scenarios also show that managing electricity demand downward (or equivalently, boosting supply) would make a much bigger difference than LNG in lowering electricity prices.

Comparing the “High Demand” and “Base Case” scenarios, lowering demand reduces both median and dry-year prices more than twice as much as achieved by the subsidised LNG. As a rough estimate, even if you could only save half the demand difference between the high and baseline scenarios, it would still come out better than LNG.

I have not seen anything in the released papers that shows that demand reduction/boosting supply was analysed for feasibility and cost. However, given the numerous reports on New Zealand’s untapped energy efficiency potential, and the huge scope for rapid uptake of rooftop solar and batteries, this seems likely to be a far lower-cost and higher-impact option than LNG.

|

| IMAGE: Christina Hood |

What now?

It’s pretty clear that further analysis is urgently needed before making a billion-dollar commitment of electricity consumer’s funds that could either be wasted or lock in higher prices than necessary.

The minister should be asking:

- With Tariki in place and providing increased gas storage for dry years, is there still any case for LNG for dry years?

- How much would demand need to reduce (or supply be boosted) to lower prices as much as LNG, and what does that cost?

- Given the large impact of Tariki and demand response, can a decision on LNG be deferred, as was the recommendation in the BCG “Energy to Grow” report?

- What other cost-effective approaches that help close the dry-year energy gap in different ways were dismissed because of overly-narrow criteria?

Finally, the government should also release all the modelling details. They have currently published scenario outputs, but not the full Concept Consulting report on the modelling, and nothing on the key assumptions such as domestic gas supply. That is needed for independent analysis of alternatives that would better meet consumers’ interests.

Christina Hood is chief advisor at the New Zealand Climate Foundation.

print this story

Story copyright © Carbon News 2026

Faster consenting, harder trade-offs

Today 12:45pm

Faster consenting is starting to produce results, but this week's decisions show speed has not removed the harder trade-offs around electricity security, conservation, ecology and climate liability.

Contact: Protected geothermal fields must be opened to meet 2040 goal

Mon 6 Jul 2026

By Oli Lewis | A goal to double geothermal energy generation by 2040 using existing technologies is unachievable unless some protected fields are reclassified for development, Contact Energy says.

Fast-track panel backs proposed Haldon Solar Farm

Mon 6 Jul 2026

By Shannon Morris-Williams | The proposed Haldon Solar Farm in the Mackenzie Basin has moved to the final stages of the Fast-track Approvals Act process after the Fast-track Panel proposed granting approval for the project.

Taranaki offshore wind developer eyes mid-2030s commissioning after law change

Fri 3 Jul 2026

By Oli Lewis | The first offshore wind farm in New Zealand could be commissioned by the mid-2030s, with its developer saying a new permitting framework has bolstered investor confidence.

EECA seeks answers on NZ's future fuel mix

Fri 3 Jul 2026

By Shannon Morris-Williams | The Energy Efficiency and Conservation Authority is looking for specialists to assess the role future low-emissions fuels could play in New Zealand’s energy system.

Australia is at least ten years ahead of us on solar. It’s time we caught up.

Fri 3 Jul 2026

By Ed Harvey | OPINION: Starting this week, millions of households across New South Wales, South Australia and Southeast Queensland will have access to three hours of free electricity every single day.

Offshore renewable energy bill passes, opening path for developers

Thu 2 Jul 2026

By Oli Lewis | Feasibility permits for offshore wind developments could be issued within months after the Government passed a long-awaited law to establish a regulatory regime.

A tale of two electricity systems as NZ and Australia roll out new cost-saving measures

Wed 1 Jul 2026

By Oli Lewis | New rules requiring electricity retailers to offer time-of-use pricing plans, where consumers can access lower-cost electricity at off-peak times, have come into effect.

Savings gap doubles: all-electric households stand to save $3000 a year, report finds

29 Jun 2026

By Oli Lewis | The economic incentive for households to electrify has become more compelling, although overcoming upfront installation costs remains a barrier.

Lake Onslow pumped hydro consortium secures funding for consent push

26 Jun 2026

By Oli Lewis | The consortium behind Lake Onslow pumped hydro has secured funding to finalise its resource consent application, aiming to lodge it under the fast-track process before 2027.