Flawed decision-making around taxing electricity to fund LNG import terminal

16 Feb 2026

By Simon Orme

COMMENT: The Government's decision to back an LNG import terminal exemplifies an egregious failure in public policy and energy sector governance.

On 9 February, the New Zealand government announced it would invest in a new liquefied natural gas (LNG) Import Facility and a supporting Cabinet paper and supporting officials’ paper (‘Exploring the case for LNG’) were published.

The papers say New Zealand needs up to 1.5TWh of additional dry-year insurance, given around 1.5TWh is deemed available from the new cartel for the Huntly steam turbines.

The paper asserts that, after consideration of feasible alternatives, an LNG import terminal is the best option for addressing the ‘dry-year’ insurance problem for energy – specifically electricity – security.

The paper proposes an accelerated procurement process ahead of the election later this year, alongside new legislation to provide consent approvals and powers to impose a new government levy on NZ businesses and families (added to or alongside an existing industry levy). Power bills for families would increase by between $15 and $30 per annum. The objective is to have the terminal operating before the winter of 2029 (3 years hence) and potentially as early as June 2027 (2 years).

An option of incentivising rooftop solar uptake across residential, commercial, and industrial uses is rejected because it: ‘Will not provide substantive additional energy during winter, when we are most likely to experience the dry-year problem.’

No regulatory impact statement (RIS) was prepared due to timeframes and uncertainty about the scope of regulatory enablement. A Quality Assurance panel finds that the limited available impact analysis partially meets quality assurance criteria. The climate boffins also took a look and gave the thumbs up.

More than two decades ago, when concerns over domestic gas production and commercial reserves first emerged, I worked as a consultant for a major regional oil and gas company on exactly this proposal. Since then, I’ve worked on gas supply, pipeline and storage pricing, infrastructure investment, LNG export and import terminals, and the implications of converting gas demand to electricity. I’ve also prepared and reviewed numerous regulatory impact statements (RIS) and supporting economic modelling.

Here’s my take on the NZ government announcement and supporting analysis: It is complete rubbish and the decision exemplifies an egregious failure in public policy and energy sector governance.

The problem definition is the guts of a RIS. Failure #1. Contrary to sound practice and guidance, there is no identification of any market failure. If LNG is the superior solution, as asserted, why is government intervention required? Why can’t the problem be fixed by the private sector? Why is a new tax required? Isn't this supposed to be a low tax, pro-market government?

The next part is to ensure all feasible options are on the table. Failure #2.

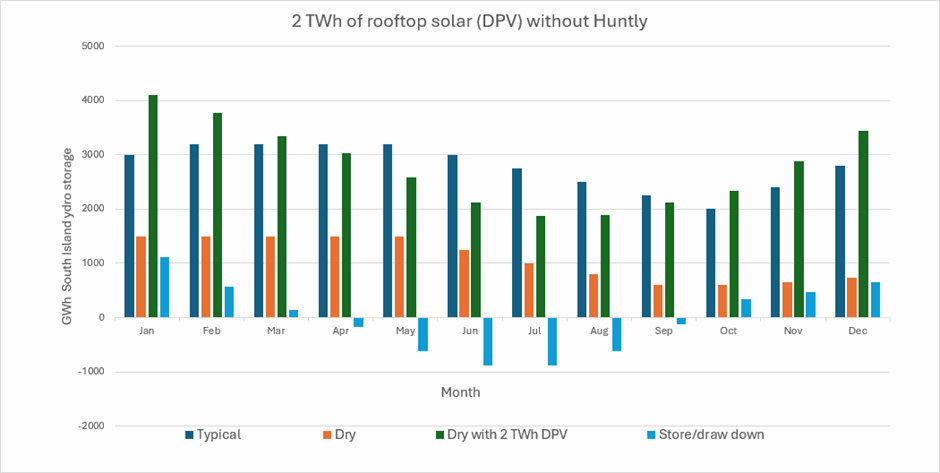

Rooftop solar is rejected because output is lower over winter when the dry year problem manifests. There seems to be no acknowledgement that NZ has 5GWh of hydro storage. The so called “inter-seasonal” energy storage problem can be addressed by 1.5GW or more of rooftop solar.

The output from this solar displaces hydro generation over summer and autumn and the existing hydro storage and capacity is more than sufficient even in a dry year. This is illustrated in the chart below, assuming 2TWh of national solar (~1.5GW of capacity).

The blue bars show the increase in hydro storage due to solar output from October through March and the draw down over April through to September, because average solar (distributed photo voltaic or DPV) output is down while average electricity demand is up. The winter draw down in the dry year scenario is manageable compared with the South Island hydro storage and national hydro generation capacity.

The key point is that daily intermittency in DPV output is not a problem given 4GWh of hydro storage in the South Island and another 1.5GWh in the North Island – plus geothermal.

Can the required rooftop capacity be built in the specified timeline? Let’s suppose, conservatively, the 2TWh output modelled above requires 1.5GW of DPV capacity.

In its latest quarterly update, the Australian Energy Market Operator notes that 13GW of rooftop solar was installed in the 5 years to the end of 2025. On average, that’s 2.6GW per annum. At Australian install rates, the required 1.5GW for New Zealand takes about 7 months.

OK, it would take New Zealand a year or two to ramp up and being smaller it probably can’t achieve Australian install rates, but 1.5GW is definitely a feasible option by 2029 and potentially earlier if afterburners were used. 3GW by say 2030 is also feasible and with 4TWh of new generation, Huntly steam and most, if not all, gas turbines could retire without jeopardizing the winter energy security margin in a dry year.

Compared with other energy infrastructure, rooftop solar is modular and inherently low risk once standards are set up and the workforce is trained up. Unlike wind and utility scale solar, there is no need for renewable energy zones and other transmission build outs. There is a very low risk of slippage in cost or commissioning dates for distributed solar compared with alternatives.

Some time and associated delay is required to design and implement a regulatory and fair pricing framework to enable a large-scale deployment of rooftop solar in New Zealand, while ensuring consumers and workers are protected. There is already a tested and proven regulatory framework in Australia that could very quickly be adapted for New Zealand. Work force training can also be ramped up quickly.

Aside from its current winter energy margin security function, gas fired generation in NZ also has a role in the North Island capacity security margin. But this capacity is also highly substitutable because the requirement is no more than 100 hours a year and they are not consecutive but in fairly short blocks over multiple days. The recent experience in Australia’s two main power markets (the national electricity market (NEM) and the Western Australian wholesale electricity market (WEM)) show that battery electric storage systems (BESS) can more efficiently provide capacity during winter peaks than peaking gas units. In New Zealand's case, even during wind and solar lulls, the hydro and geothermal capacity allows for BESS to be recharged for the following evening winter peak.

What would the LNG bill impact be? This is failure #3 - there is no proper impact assessment.

The impact of the rejected solar option is vastly better than the modelled outcomes. This is because 2TWh of zero marginal cost solar means that hydro storage and output would no longer be valued relative to high-cost output from coal and gas. Wholesale prices would be structurally and persistently reduced.

The financial impact could, however, be substantial because, under international accounting rules, the currently inflated value of forward wholesale contracts, and hydro-storage and generating assets, would need to be written down. This would impact profits, dividends and taxes paid – and hence the Government’s deficit and borrowing requirement. But this is a transitional problem and is not the main game in a proper RIS and economic business case. The bigger the short-term financial impact, the bigger the long-term economic gain to national competitiveness and affordability.

The Government is seeking to contract for an inferior infrastructure option ahead of the national election later this year.

The outcome of the election is of course uncertain, and one can only hope that an incoming government of whatever complexion places priority on protecting and enhancing national competitiveness and energy affordability for kiwi businesses and families.

A new government could decide to do what the current government did with a contract for purchasing new ferries, shortly after coming to office.

Simon Orme is an Australian based Kiwi born energy expert (Ngāti Awa, Ngāti Tarāwhai). He is a former New Zealand Treasury official. He worked on Huntly fuel supply in the 1990s, gas imports in 2002-03, and recently on raising capital for a large portfolio of real zero grid scale generation storage, and rapid deployment of rooftop solar at scale. He advises investors, developers, governments and others on the energy transition in Australia and elsewhere. Recent and ongoing projects include designing and implementing the roadmap for replacing 9GW of coal generation in NSW, decarbonising the Pilbara energy system, reforming the wholesale electricity market in Western Australia, and accelerating consumer energy resources including rooftop solar.

print this story

Story copyright © Carbon News 2026

Hipkins pans LNG plan as ‘massive step backwards’

Tue 19 May 2026

By Liz Kivi | Labour leader Chris Hipkins has told a Queenstown audience that a Government he leads would not proceed with a planned LNG import terminal, if elected at November’s election.

Competition weak in key energy sectors says Commerce Commission

Tue 19 May 2026

The Commerce Commission says competition remains weak in New Zealand's electricity and gas sectors despite modest improvement across the wider economy, highlighting how difficult it is for new entrants to challenge established infrastructure players.

Biomass sector asks: where did the love go?

Mon 18 May 2026

By Pattrick Smellie | New Zealand has sufficient biomass in its plantation forests to replace natural gas for industrial process heat at lower costs than electrification, but is failing to get the attention it deserves, sector leaders say.

Mercury eyes $1b geothermal expansion near Taupō

Fri 15 May 2026

Mercury is planning the next phase of its geothermal expansion near Taupō, with two proposed projects carrying a potential investment of up to $1 billion and enough new renewable generation to power an additional 125,000 homes.

World Nuclear Association chief to address NZ energy conference

Thu 14 May 2026

The head of the World Nuclear Association will speak at a Hamilton energy conference as debate grows over whether emerging nuclear technologies could play a role in New Zealand’s future energy mix.

GIDI-style help cheaper than LNG: MBIE

11 May 2026

By Pattrick Smellie | Officials advised ministers last July that the lowest-cost way to free up gas for use during dry winters was to assist industrial gas users to switch to electricity.

Govt launches solar red tape review to speed up installations

8 May 2026

By Shannon Morris-Williams | The Government has launched a review aimed at making residential and small-scale solar installations faster and easier, in a move Rewiring Aotearoa says could help cut costs and accelerate solar uptake across New Zealand.

Energy system debate to headline Electrify Queenstown

7 May 2026

A major political debate on the future of New Zealand’s energy system will take centre stage at Electrify Queenstown 2026, as policymakers and industry figures gather to map the country’s path toward electrification.

Methanexit: writing on the wall for NZ’s biggest gas user

6 May 2026

By Liz Kivi | New Zealand’s biggest fossil gas user, Methanex, is expected to stop production by the end of this year, with the company confirming its Motunui methanol operation won’t survive Māui gas field’s closure.

Ōmokoroa trial to test smarter power use

6 May 2026

Powerco and Energy Efficiency and Conservation Authority are launching a trial in Ōmokoroa, Bay of Plenty, to test how shifting electricity use away from peak times could ease pressure on the network and reduce costs.