If the government is set on an LNG terminal, gas users, not electricity users, should pay

11 Mar 2026

By Christina Hood

COMMENT: It's increasingly clear that the government's narrative of LNG as ‘dry year electricity insurance’ really doesn't stack up.

The Government’s own analysis shows there are lower-cost pathways for electricity.

While the Government has promoted the LNG facility as a dry year ‘insurance policy’ to prevent wholesale electricity spot prices peaking to extreme levels during dry winters, both the Energy Minister and the Cabinet papers mention “spillover benefits” including the ongoing availability of gas for industrial users who face sharply declining supplies of domestic natural gas.

If the LNG import terminal is actually about backstopping gas supply for gas users, gas users should pay for it. To the extent that electricity generators use gas, they would pay their share as a gas user.

There therefore needs to be a transparent discussion on:

1) what LNG would cost gas users without cross-subsidy from the rest of the economy

2) how long gas users would be locked into paying levies

3) whether there are cheaper and better options to balance supply and demand in the gas market (like proactively helping users to transition off gas to electric heat pumps or biomass, which experts say has significantly higher potential than the government assumes for rebalancing the market), and

4) whether gas users collectively want to go ahead with LNG or not on that basis.

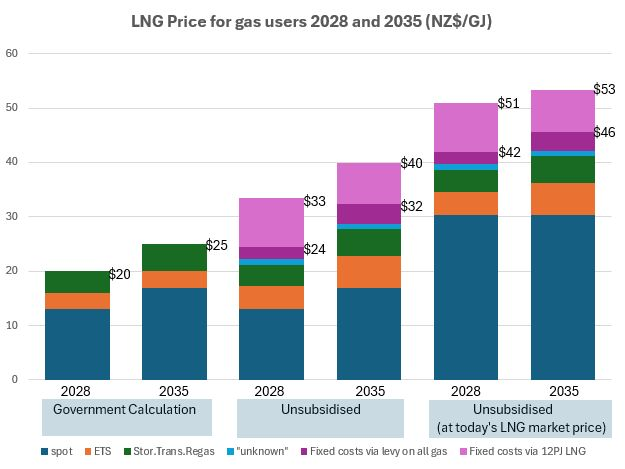

The graph below gives a quick look at LNG unit costs:

The government's modelling (left two columns) used NZ$20/GJ in 2028 ($13 spot, $3 ETS, $4 transport, storage, and regasification), and NZ$25 in 2035 ($17 spot, $3 ETS, $5 TSR).

But the government's numbers assume:

-

the ETS remains toothless out to 2035 and ETS prices stay at $55. It seems to me rash to plan on that basis: in the centre two columns I've instead used the ETS auction floor price track, which is still conservative. If we get the ETS back on track, the price will be higher.

-

"unknown" costs flagged in the government papers (premium for spot sales, extra transport from some destinations, bespoke processing) are ignored. I've put in $1/GJ as a placeholder.

-

someone else pays for the fixed costs of the LNG terminal. I've put in two options for gas users covering costs without that subsidy: in dark purple a levy across all gas use, and in light purple cost recovery on each unit of LNG directly, based on 12PJ/yr imports (for fixed $135M/yr). The levy on all gas increases over time, as costs are shared across a shrinking pool of users.

Finally, in the right two columns I've shown a version with the international LNG price at yesterday's closing levels, to highlight what price spikes can do.

At long-run projected LNG prices, that puts the delivered cost of LNG at around NZ$24/GJ in 2028 and $32/GJ in 2035 if fixed costs are recovered by a levy on all gas use. But supply disruptions could spike that well above $40/GJ. If international LNG spot prices are passed directly through to consumers as is the case for petrol and diesel, then that risks high volatility in domestic energy prices. On the other hand if gas suppliers hedge import LNG prices, that would add a further margin to costs every year that is not in MBIE’s calculations.

This again points to the core question: do gas users actually want to commit to $25-$30/GJ gas for 15 years, or will there be insufficient demand given that many have switching alternatives (which in turn eases market pressure for those who do not). That analysis has not been presented: there seems to be a false assumption that gas demand continues whatever the price. That’s not a basis for a $2.7 billion commitment - the analysis needs to be done and debated in the open before decisions are locked in.

|

| Image: Christina Hood/Compass Climate |

Christina Hood is chief advisor at the New Zealand Climate Foundation.

print this story

Story copyright © Carbon News 2026

Announcements expected soon on $200M gas fund

Fri 24 Apr 2026

By Pattrick Smellie | Fossil fuel companies appear likely to take up a $200 million government fund to encourage additional oil and gas exploration, dashing lobbyist Business New Zealand’s hopes that it might be repurposed to underwrite industrial electrification.

Going concern status flags depth of Methanex NZ's gas crisis

Tue 21 Apr 2026

Methanex's New Zealand operation is relying on financial support from its Canadian parent to remain a going concern after a second consecutive year of asset impairments left the business with negative equity.

Diesel crunch exposes fuel vulnerability

Mon 20 Apr 2026

By Shannon Morris-Williams | Rising diesel prices and tightening supply are exposing New Zealand’s heavy reliance on fossil fuels, with experts warning the squeeze on farming and forestry is likely to ripple through the economy while strengthening the case for lower-emissions energy alternatives.

Marlborough’s Rānui Solar Farm enters final testing

16 Apr 2026

By Shannon Morris-Williams | Marlborough's biggest solar farm has entered its final testing phase and is now generating up to 9.9MW of electricity, marking a key milestone for a project expected to boost regional energy security.

Pūkaki consent battle becomes proxy for system risk

14 Apr 2026

The fight over Lake Pūkaki is no longer just about a consent change. It has become a proxy for how much New Zealand is willing to pay for electricity system resilience – and how that price should be set.

Global uncertainty driving solar surge

13 Apr 2026

By Shannon Morris-Williams | Global instability and rising energy costs are pushing more New Zealanders towards solar, with companies reporting a surge in enquiries as households look for greater control and resilience in an increasingly uncertain energy landscape.

New alliance wants renewable-led energy – and Govt to press pause on LNG

9 Apr 2026

A newly formed coalition of business, consumer and energy organisations has unveiled a renewable-led strategy it says will strengthen the country’s energy security, and it’s calling on the Government to pause its plan for an LNG import terminal.

Genesis fires up pellet study with Nature’s Flame

8 Apr 2026

By Pattrick Smellie | Genesis Energy is extending its quest for locally produced torrefied wood pellets to supplement coal and gas to fuel its Huntly power station, announcing it is investigating plant construction with established local solid fuels player Nature’s Flame.

EA entrenches 10kW export limit for residential solar

8 Apr 2026

By Pattrick Smellie | The Electricity Authority intends to require all electricity networks to offer at least a 10 kilowatt (kW) export capacity for residential rooftop and other small-scale distributed generation.

Renewable build-out runs into grid and firming limits

8 Apr 2026

New Zealand's electricity market entered 2026 with renewable generation at record levels and a substantial build pipeline finally moving from paper to construction. The harder question is whether the wider system can absorb and firm that capacity fast enough.