Is a storm brewing for NZ dairy production?

22 Apr 2024

|

| PHOTO: Bernd Dittrich on Unsplash |

By Nick Swallow

OPINION: Animal proteins make up 40% of New Zealand’s exports. So why aren’t we talking about alternative proteins, which look set to disrupt the dairy industry along with a major source of our country’s wealth?

The Our Land and Water report “Protein Futures: Future Scenarios for Land Use in Aotearoa New Zealand. Synthesis Report” was released on the 27th of March. Don’t be fooled by the unimaginative title, this is an important document for the future of New Zealand’s economy, trade, and well our wealth as a nation in general.

The 66-page report investigates the impact of alternative protein production on New Zealand’s agriculture through to 2035. Animal proteins are a big deal for our country as they make up more than 40% of our exports, principally through dairy, beef, and sheep meat. This is where our wealth as a nation is generated. Disruption to this wealth generation is a disruption to the quality of life we enjoy.

The alternative protein sources in the research are broken into three groups (i) plant-based (oat milk, etc.), (ii) cellular agriculture (printing meat in labs), and (iii) precision fermentation (PF). It’s the last one, precision fermentation that steals the show. PF uses micro-organisms in controlled environments to produce proteins. If you’ve seen a beer brewery, it’s like that, but the output isn’t brown and frothy, but rather white and powdery dairy protein.

PF is already used to make proteins, 80% of rennet, critical to making cheese, comes from PF, as does the insulin diabetics use. Rennet and insulin were obvious options for an alternative means of production as they were extracted from problematic sources – notably cow stomachs and pig pancreases. It was a messy, costly, and inefficient business. Now the sights are set on dairy, and the prize is huge.

Fermenting the future of protein

Why does PF steal the show? Because of its ability to disrupt New Zealand’s dairy industry. While NZ only accounts for 3% of global production, 95% of our dairy is exported, and we contribute to about 30% of global dairy exports. Dairy produced in other countries is often drunk as fresh milk in that country, or nearby.

New Zealand is far from our export markets, and 87% of milk is water. Shipping water is expensive, so 74% of New Zealand milk is spray-dried and sent offshore in bags where it goes into global food supply chains. We’re good at this, dairy exports tripled between 2004 and 2020, making up one in four of every export dollar NZ earns.

Through PF, the components of dairy have started to be produced commercially on a small scale. Last month Nestlé released Better Whey, a whey protein powder made through PF. Daisy Labs, a New Zealand company, is working on producing lactoferrin (a high-value whey protein found in cow milk) using the process. Many other initiatives are happening globally to produce dairy proteins – each has the potential to remove some part of the value extracted from milk.

There are barriers to production using PF, which the report acknowledges, such as scaling the technology and the need for investment. There will also be regulations to overcome. It’s not a large-scale commercial technology… yet.

The global context behind our biggest export

The report highlights that in 2022 alternative protein production received $2.9b in investment. A share of this money will be chasing the prize of disrupting the $893b US dairy market. There are clear drivers for investment into producing dairy ingredients from PF, which are mentioned in the report.

-

Sustainability outcomes. Reductions in greenhouse gas (GHG) emissions, nitrogen, and phosphorus entering the environment and their damaging impacts. PF is touted as a lower emissions means of production, a ReThinkX report in 2019 predicts a 90% reduction in GHG emissions from agriculture using PF and cellular agriculture by 2035.

-

Market forces for emissions reductions. Large food producers such as Nestlé, Mars, Pepsi, Danone, etc. all have significant commitments to reducing the GHG emissions in their supply chains – called “scope 3 emissions”. Dairy is the largest source of Nestlé’s scope 3 emissions and PF is an obvious technology to support them in reaching their goals.

-

Cost savings. The promise of PF is price parity for production in the near future, estimates are from 2026 to 2030. Once reached, scaling the technology would allow for lower prices. While the capital anticipated to make this commercial is significant, so too is the capital currently invested in producing milk on farms.

-

Food security and increasing demand for protein. With a rising population and complexities in geopolitics, the allure of bringing protein production, at scale, inside countries is considerable. The UAE is building a PF plant to make casein, the protein that makes cheese gooey. They plan to be cow-free exporters of proteins, from the advantage of being well placed geographically.

A $25 billion loss to the economy and counting?

The report looked at the impact of increasing PF production on New Zealand land use. It models three scenarios against a business-as-usual baseline. At the “high” scenario where PF of dairy products becomes competitive, it displaces 22% of global dairy production, which contributes to a 35% reduction in land used for dairy by 2035. The report claims that land-use changes will not be significant by 2035, I can’t imagine how a 35% reduction in dairy land in New Zealand isn’t significant.

The report doesn’t take the step of quantifying the loss of capital, but it does show a reduction of 725,000 hectares of dairy farming, replaced by 601,000 hectares of beef farming, and the remainder in arable. Currently, a hectare of a dairy farm sells on average for $39.2k (according to Real Estate NZ), whereas sheep and beef farms sell for an average of $10.3k (according to Property Brokers).

That’s a $28.9k differential at today’s value, modeling the shift from dairy would devalue the land by $17.4 billion. The report predicts an $8 billion loss to the New Zealand economy – it’s not clear from the report if this is total, or per annum. This means we’re up to about $25 billion by 2035, without considering stranded assets, such as milking sheds, wintering barns, or milk drying plants, nor the impact on funders.

Extrapolating the trajectory of the disruption curve used by the researchers shows that the PF pathway for dairy proteins is steep up until 2035 (where the modeling stops), it’s likely a 22% displacement won’t be the ceiling. Given the four drivers outlined earlier, why would it stop? Should this level of displacement be reached, further disruption is surely inevitable. Given all this, the $25b reduction is likely to be more considerable over time.

How likely is a PF to replace 22% of dairy by 2035?

This is the critical question here, and predicting the future is notoriously fraught. The approach in the report was to use the scenarios and model those using the Lincoln Trade and Environment Model (LTEM). This is a mathematical model that predicts what may happen based on various inputs.

Where there is a concerning limitation in this research is the inputs for the scenarios, i.e. the predictions of the uptake of alternative proteins. The researchers used one paper from Boston Consulting Group (BCG) released three years ago as the input to modeling the scenarios. The paper is not peer-reviewed and is scant in detail about how BCG arrived at its predictions. The scenarios are based on one graph in the paper that has as its sources “Blue Horizon and BCG analysis” – that’s it. Blue Horizon is an investment company, who knows what “BCG analysis” means? The BCG team doesn’t expand on that in the report.

To their credit, the authors of the Kiwi report mention they contacted BCG to discuss the report, but there was no mention of what their conversation clarified. From my reading of the report, the Kiwi researchers didn’t take the step of having the BCG approach peer-reviewed by experts. There are alternative reports on this topic, for example, a ReThinkX report predicts a 90% of US dairy production to come from PF alternatives by 2030.

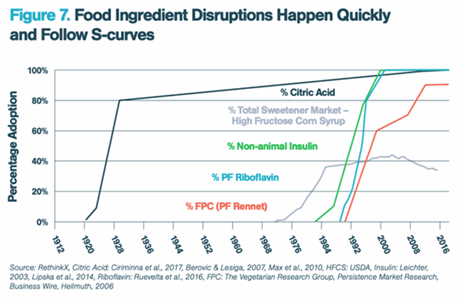

Considering the implication of these scenarios to the outcome of the report, this limitation is significant, and the rapid “s-curve” adoption of other PF food disruption (see the figure below), suggests 22% replacement by 2035 might be an understatement even at the highest scenario.

Given the reliance on the scenarios, are we betting the farm (pardon the pun) on sound information? And given the significance of the losses to the New Zealand economy by 2035 at the “high” scenario, should we rely on this one report as the input? Further research needs to be done to develop credible scenarios for modeling.

What bubbles out of this report?

The warning to NZ’s future found in this report is clear, the threat to our means of wealth production is significant enough to warrant a response. We need to be discussing this and we need a plan for how we cope with reduced demand for dairy production from cows. Our future depends on the plans we make today to innovate and adapt to this future.

Nick Swallow is a former New Zealand Trade and Enterprise’s (NZTE) Trade Commissioner to the UK and Ireland and has a Masters of Sustainability Leadership from the University of Cambridge, completing his dissertation on dairy farming in New Zealand. Nick is currently a director at KPMG working in sustainability, however the views expressed here are his own.

print this story

Climate Leaders Coalition on PM meetings: 'it wasn’t us'

Mon 25 May 2026

By Pattrick Smellie | The 81-member Climate Leaders Coalition is distancing itself from the actions of members who lobbied the Prime Minister’s Office to intervene and stop a landmark climate change court case.

Corporate coddling is killing our climate

Mon 25 May 2026

By Matt Halliday | COMMENT: The New Zealand Government’s recent move, undercutting citizens’ rights and the rule of law to cancel the country’s most important climate case, Smith v Fonterra, is a massive victory for corporate lobbying.

Mike Smith’s asymmetric victory

Mon 25 May 2026

By Pattrick Smellie | COMMENT: The New Zealand Government’s recent move, undercutting citizens’ rights and the rule of law to cancel the country’s most important climate case is a massive win for Mike Smith, the climate change activist who brought it.

Govt ramps up war on wilding pines with $79m boost

Mon 25 May 2026

By Shannon Morris-Williams | The Government is ramping up efforts to contain the spread of wilding pines with a $79 million funding boost aimed at protecting farmland, biodiversity hotspots, tourism landscapes and water catchments across New Zealand.

Rotorua extends diesel bus contract after NZTA declines extra funding

Mon 25 May 2026

By Mathew Nash, Local Democracy Reporter | Rotorua is stuck with its diesel-powered public buses after a funding snag played a part in setting back plans for zero-emission buses by years.

Marae solar project boosts sustainability and mana motuhake

Mon 25 May 2026

By Moana Ellis, Local Democracy Reporter | Five marae from Whanganui to Taumarunui are running on solar power and many more could join a major green energy initiative aimed at cutting electricity costs and strengthening community resilience.

Govt had ‘little choice’ in signing key UN climate resolution – expert

Fri 22 May 2026

By Shannon Morris-Williams | Climate policy expert Bronwyn Hayward said it was “shameful’ New Zealand didn’t throw more active support behind a pivotal climate resolution ratified by the United Nations this week.

NZ at risk of falling behind on EV transition

Fri 22 May 2026

By Shannon Morris-Williams | An EV lobby group is warning that New Zealand is at a crossroads on transport electrification, with inconsistent policy settings and lagging charging infrastructure slowing uptake, while global adoption accelerates and fuel price shocks renew interest in electric vehicles.

New DOC chief appointed as public sector cuts loom

Fri 22 May 2026

By Shannon Morris-Williams | Peter Chrisp has been appointed the new Director-General of Conservation, just as the Department of Conservation again finds itself in the firing line of the Government’s public sector cost-cutting programme.

Media round-up

Fri 22 May 2026

In our round-up of climate coverage in local media: Shane Jone is urging mining bosses to apply for fast-track before the election, climate risk is changing where investors put their money, and Hiringa gets more hydrogen-fuelled trucks on the road.