Is extending Huntly power station to 2035 in consumers’ best interest?

22 Jul 2025

By Simon Orme

COMMENT: Genesis Energy is proposing a cartel to keep high-emitting Huntly Power Station in business to 2035. If extending Huntly has economic benefits, is a cartel necessary?

New Zealand faces a major decision impacting its future energy competitiveness, affordability, and security. While most power generation has close to zero marginal cost and emissions, the small volume of remaining high-cost thermal electricity generation is a key factor behind excessive power prices.

Last winter, low hydro inflows coincided with long anticipated declines in Taranaki gas production. This resulted in demand curtailment, a price spike and higher forward prices.

High power prices and reduced demand contributed to the GDP decline in the year to March 2025. High forward prices are a continuing economic drag.

New Zealand has ample energy resources. There are willing investors with large and diverse planning-approved zero emissions projects with very low marginal costs. Along with hydro generation, wind and solar generation have zero fuel costs and zero carbon emissions (‘real zero’). If most of the proposed new real zero generation pipeline went ahead, forward wholesale electricity prices would fall, and energy security would be improved. But all but 5.9% of the pipeline remains uncommitted.

Proposal to extend Huntly to 2035

On 18 June, Genesis Energy announced initial multilateral contracts with Mercury, Meridian and Contact (recently merged with Manawa). These non-binding contracts are steps toward extending operation of the remaining three steam units at the 43-year-old Huntly power station to 2035. The group of four (plus Manawa) developing the Huntly proposal for possible authorisation now controls 97% of New Zealand’s generation.

Cartel requires authorisation

A cartel is where a group of businesses act together instead of competing. The Commerce Act prohibits contracts, arrangements or understandings substantially reducing competition.

Genesis needs authorisation from the Commerce Commission (ComCom), to finalise a set of new long-term agreements for access to Huntly output, by November. According to ComCom, ‘[e]ven if the agreement is not put into practice, the act of reaching (or attempting to reach) an anti-competitive agreement is also illegal.’

If these electricity contracts are finalised and approved, Genesis can then secure long term fuel supplies for Huntly in time for winter 2026, sufficient to defer gradual retirement of all three units. One of the torrefied wood projects, that would replace imported coal and Taranaki gas from around 2028, has already been blessed under the Fast Track Approval Process.

At the end of June, ComCom confirmed it had engaged with Genesis and is expecting an application for an authorisation “soon”. At the time of writing, no application is listed by ComCom.

Authorisation of a cartel under Section 58 of the Commerce Act is possible only if the applicant can demonstrate the harms of restricting competition are outweighed by the benefits. A KPMG/Concept Consulting report commissioned by Genesis concludes that, without the Huntly units, wholesale electricity prices would likely be 60% higher over the period to 2028 and up to 11% beyond that.

This conclusion is based on modelling and input assumptions. The nature and cost of the alternatives to extending Huntly have so far not been market tested.

While a cartel would restrict competition, it won’t be a closed shop. Spare Huntly capacity would be made available to businesses outside the cartel. This may become mandated under proposals being developed jointly by ComCom and the Electricity Authority.

Real zero probably better than high emissions renewables

The announced intention to seek authorisation for a cartel does not inspire confidence there are net benefits from extending Huntly. If there were net benefits, Huntly could outcompete alternatives all the way to 2035.

Ahead of Genesis submitting its application, extending Huntly to 2035 seems unlikely to be the lowest cost feasible option. Huntly’s advantage is its costs are depreciated, whereas replacement generation incurs new depreciation and financing costs.

Switching to torrefied wood production also incurs new depreciation and financing costs. From international comparisons, the cost of torrefied wood is likely to be in the range of NZ $12-$18/GJ. This is a big cost increase compared with similar quality Indonesian coal. Genesis is understandably seeking to pool the risk across as much of the market as possible. That’s because the competitive threat to Huntly is real.

The feasible timeline for delivering new real zero energy and capacity to replace the Huntly units is similar to the timeline for switching Huntly to biomass – 24 to 36 months.

Since the last public study of the economics of replacing Huntly in 2019, real zero costs have fallen globally. This reflects the global ramp up of real zero energy output.

New real zero energy costs and energisation timelines in NZ can be reduced further by adopting international innovations. These include: mass adoption of rooftop solar; renewable energy zones to reduce grid solar and wind connection delay and cost; and long-term energy supply agreements to reduce financing costs. Taken together, these innovations could mean Huntly’s steam units would become stranded assets well before 2035

Around 72% of the core proposed new real zero generation pipeline (onshore wind and grid solar only) is independent from the would-be cartel members. The equivalent generation proposed by the would-be cartel is 28% of the total.

Even if real zero has a longer lead time, running Huntly on coal for another year or so is probably better than running it on biomass for an additional six or seven years.

Biomass may be renewable, but emissions costs are similar to coal

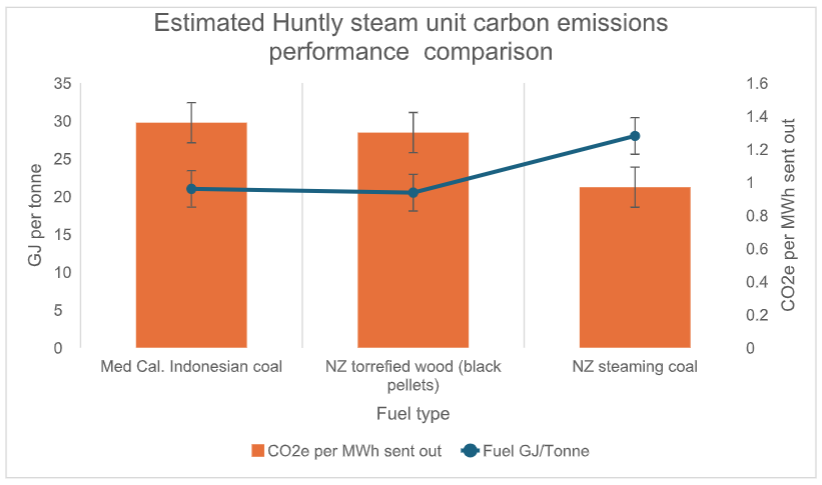

Proponents of torrefied wood and other biofuel options highlight wood can be replaced. Switching Huntly from coal to renewable fuels does not in fact avoid high emissions and carbon offset costs. The chart below compares energy density across different fuels (LH axis) and the resultant carbon emissions (RH axis) exceed 1 tonne per MWh sent out from Huntly.

|

| Sources: Genesis, Indonesian, and domestic coal and torrefied wood suppliers (with performance improvement for black vs. US white pellets.) The chart draws on limited publicly available data and are modelled estimates only. While the values in the Y axes may vary, the relative emissions from different fuels is largely determined by fuel quality, not source. |

Total domestic emissions from torrefied wood are significantly higher than indicated here, due to the energy required for the torrefaction process – heating the wood to between 200C and 300C. Further energy and emissions are created from transporting dispersed forestry slash to torrefaction plants and then to Huntly.

The emissions from torrefied wood combustion must be offset with New Zealand or international carbon certificates. Relative to 2050 Nationally Determined Contribution carbon budgets, the additional emissions from extending Huntly from say 2028 to 2035 entails an increase in total national emissions abatement costs. This cost increase is on top of the higher cost of the torrefied fuel.

Impact of replacing Huntly on hydro output and unit prices

The value of extending Huntly for members of the would-be cartel is that it has the least displacement of their other generation. Outside dry years, Huntly output can be the minimum required to maintain steam units and manage fuel stocks.

By contrast, new large scale, real zero, independent generation would seek to operate at full output during normal years. This could displace current hydro energy generation and revenues outside winter, and result in larger and more frequent spills. Hydro generators would have less opportunity to shadow price against high-cost thermal generation – whether coal, gas, wood or biomethane fired.

Hydro assets remain critical to system reliability and security. This reflects their quick start, high dispatchable capacity, supply of essential system services, and ability to maintain high output during extended high demand, low real zero generation periods.

Addressing the influence of the would-be cartel members is critical to large scale entry of new real zero generation.

‘But we can’t store wind and solar energy’

With sufficient new real zero generation, in diverse locations, some remaining gas fired units, and committed and possibly new battery energy storage systems, winter energy and capacity margins can be maintained post Huntly exit. Even during consecutive dry years, the current ~4.5TWh of hydro energy storage provides a massive buffer for winters and any other times when demand is much higher than average, while combined new real zero output is lower than average.

A key driver of the winter energy shortfall problem during dry years is that hydro storage is currently being used to produce energy throughout the year. With a lot more real zero generation output throughout the year, hydro energy output could instead be shifted to the winter and other times when it has the highest value. There would be more hydro spill, but the opportunity cost of the spilled energy would no longer be linked to high-cost thermal energy.

Releasing the rooftop solar disrupter from its chains

Rooftop solar is not identified as a feasible Huntly replacement option in all public assessments of replacing Huntly, including the 2025 KPMG report for Genesis. Falling capital costs and avoided fuel and emissions costs together mean that solar is likely to be lower cost than extending Huntly.

The fastest, lowest cost replacement for Huntly is at least 2TWh of rooftop solar by 2028. In most parts of New Zealand, rooftop solar is the lowest cost energy at the point of demand. It does not require network augmentations or fast track planning approvals and can be scaled up to 4TWh by 2030. The grid is sized for winter evening peaks. Solar uses spare grid capacity during sunny days.

What’s next?

The proposal to form a cartel implies better alternatives could be available. Genesis may be timing its application to ComCom to align with Government decisions ahead of the release of the Draft Report for the Review of Electricity Market Performance.

Extending Huntly to 2035 is a high cost, high emissions counterfactual. It will be challenging for Genesis to demonstrate that its proposal is lower cost than feasible alternatives, given these have not been market tested.

Renewable energy does not always mean low emissions energy. Genesis needs to demonstrate that it has fully identified and evaluated counterfactuals other than extending Huntly to 2035, including a rooftop solar rollout at scale 2-4 TWh scale.

Simon Orme is an Australian based Kiwi born energy expert (Ngāti Awa, Ngāti Tarāwhai). He is a former New Zealand Treasury official. He worked on Huntly fuel supply in the 1990s, gas imports in 2002-03, and recently on raising capital for a large portfolio of real zero grid scale generation storage, and rapid deployment of rooftop solar at scale. He advises investors, developers, governments and others on the energy transition in Australia and elsewhere. Recent and ongoing projects include designing and implementing the roadmap for replacing 9GW of coal generation in NSW, decarbonising the Pilbara energy system, reforming the wholesale electricity market in Western Australia, and accelerating consumer energy resources including rooftop solar.

print this story

Story copyright © Carbon News 2025

Faster consenting, harder trade-offs

Today 12:45pm

Faster consenting is starting to produce results, but this week's decisions show speed has not removed the harder trade-offs around electricity security, conservation, ecology and climate liability.

Contact: Protected geothermal fields must be opened to meet 2040 goal

Mon 6 Jul 2026

By Oli Lewis | A goal to double geothermal energy generation by 2040 using existing technologies is unachievable unless some protected fields are reclassified for development, Contact Energy says.

Fast-track panel backs proposed Haldon Solar Farm

Mon 6 Jul 2026

By Shannon Morris-Williams | The proposed Haldon Solar Farm in the Mackenzie Basin has moved to the final stages of the Fast-track Approvals Act process after the Fast-track Panel proposed granting approval for the project.

Taranaki offshore wind developer eyes mid-2030s commissioning after law change

Fri 3 Jul 2026

By Oli Lewis | The first offshore wind farm in New Zealand could be commissioned by the mid-2030s, with its developer saying a new permitting framework has bolstered investor confidence.

EECA seeks answers on NZ's future fuel mix

Fri 3 Jul 2026

By Shannon Morris-Williams | The Energy Efficiency and Conservation Authority is looking for specialists to assess the role future low-emissions fuels could play in New Zealand’s energy system.

Australia is at least ten years ahead of us on solar. It’s time we caught up.

Fri 3 Jul 2026

By Ed Harvey | OPINION: Starting this week, millions of households across New South Wales, South Australia and Southeast Queensland will have access to three hours of free electricity every single day.

Offshore renewable energy bill passes, opening path for developers

Thu 2 Jul 2026

By Oli Lewis | Feasibility permits for offshore wind developments could be issued within months after the Government passed a long-awaited law to establish a regulatory regime.

A tale of two electricity systems as NZ and Australia roll out new cost-saving measures

Wed 1 Jul 2026

By Oli Lewis | New rules requiring electricity retailers to offer time-of-use pricing plans, where consumers can access lower-cost electricity at off-peak times, have come into effect.

Savings gap doubles: all-electric households stand to save $3000 a year, report finds

29 Jun 2026

By Oli Lewis | The economic incentive for households to electrify has become more compelling, although overcoming upfront installation costs remains a barrier.

Lake Onslow pumped hydro consortium secures funding for consent push

26 Jun 2026

By Oli Lewis | The consortium behind Lake Onslow pumped hydro has secured funding to finalise its resource consent application, aiming to lodge it under the fast-track process before 2027.